Zendesk says they have a clear path to hitting $3.4 billion in revenue by 2025.

Nearly double its current $1.93 billion…But can it actually get there?

In 2021, Zendesk grew revenue by 30% to $1.34 billion. It had over 170,000 customers, including Airbnb, Shopify, and Uber, and was seen as the leader in customer service software.Then:

- Stock dropped 45% in 2022.

- Activist investors pushed for a sale, calling Zendesk mismanaged.

- The company tried to sell itself—twice—but couldn’t find a buyer.

- Private equity stepped in and bought Zendesk for $10.2 billion, taking it off the public markets.

Now, Zendesk is rebuilding under private ownership.

It’s betting big on AI automation, enterprise customers, and expanding its platform to regain momentum and nearly double revenue in three years.But does that plan hold up?

Is $3.4 billion in revenue realistic, or is Zendesk overpromising?

Let’s look at how Zendesk got to $1.9 billion—and whether it has the strategy to reach $3.4 billion by the end of this year.

First we’ll go over some statistics:

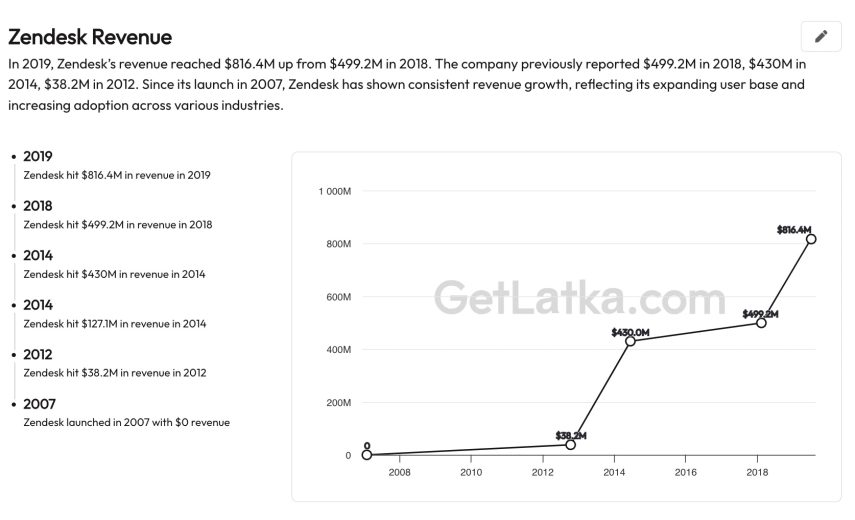

What is Zendesk’s Revenue?

Zendesk’s revenue reached $1.93 billion in 2024.

| Year | Revenue |

|---|---|

| 2007 | $0 |

| 2015 | $208M |

| 2017 | $431M |

| 2019 | $816M |

| 2021 | $1.34B |

| 2022 | $1.58B |

| 2023 | $1.75B |

| 2024 | $1.93B |

What is Zendesk’s Valuation?

Zendesk’s valuation is $9.62 billion as of 2024.

Who is the CEO of Zendesk?

The CEO of Zendesk is Tom Eggemeier.

Who Are Zendesk’s Competitors?

Zendesk’s main competitors include HubSpot, Intercom, Zoho Desk, Help Scout, LiveAgent, and Salesforce.

How Did Zendesk Reach $1.93 Billion in Revenue?

Zendesk’s revenue has grown steadily over 17 years, reaching $1.93 billion in 2024. But the way it makes money today looks very different from when it started.

At first, Zendesk focused on small and mid-sized businesses (SMBs), offering a simple and affordable customer support tool. That worked for a while, but SMB customers churn too often—meaning they switch tools frequently, making revenue unpredictable.

Zendesk realized the real money was in enterprise deals—large companies willing to pay for customized solutions, AI-powered automation, and hands-on support.

That shift completely changed its business model.

What’s Driving This Growth?

- Enterprise customers – More than 50% of Zendesk’s revenue now comes from big companies on long-term contracts.

- AI and automation – Zendesk added AI-powered tools to help businesses reduce support costs and improve efficiency.

- Professional services – Large clients need more than just software; they pay Zendesk for custom integrations and dedicated support teams.

Why Zendesk Shifted from SMBs to Enterprise Customers

When Zendesk first launched, it built its brand around startups and small businesses. But over time, SMBs proved to be unreliable customers.

Here’s why:

| SMB Customers | Enterprise Customers | |

|---|---|---|

| Contract Size | $500-$5,000/year | $50,000-$500,000/year |

| Churn Rate | High (switch tools often) | Low (locked into multi-year deals) |

| Revenue Impact | Unstable, requires high volume | Fewer accounts, but steady revenue |

Zendesk made a deliberate decision to go after enterprise customers, knowing that:

- Large companies don’t switch software as often

- Bigger contracts mean more predictable revenue

- AI-powered automation is more valuable for companies handling millions of customer interactions

This move made Zendesk’s revenue more stable, less reliant on chasing new customers, and ultimately more profitable.

4 Revenue Streams

1. Subscription Revenue (Core Business Model)

Just like all of the successful SaaS companies such as Figma and Grammarly, Zendesk does so well with a subscription model.

Zendesk’s subscription 85% of total revenue.

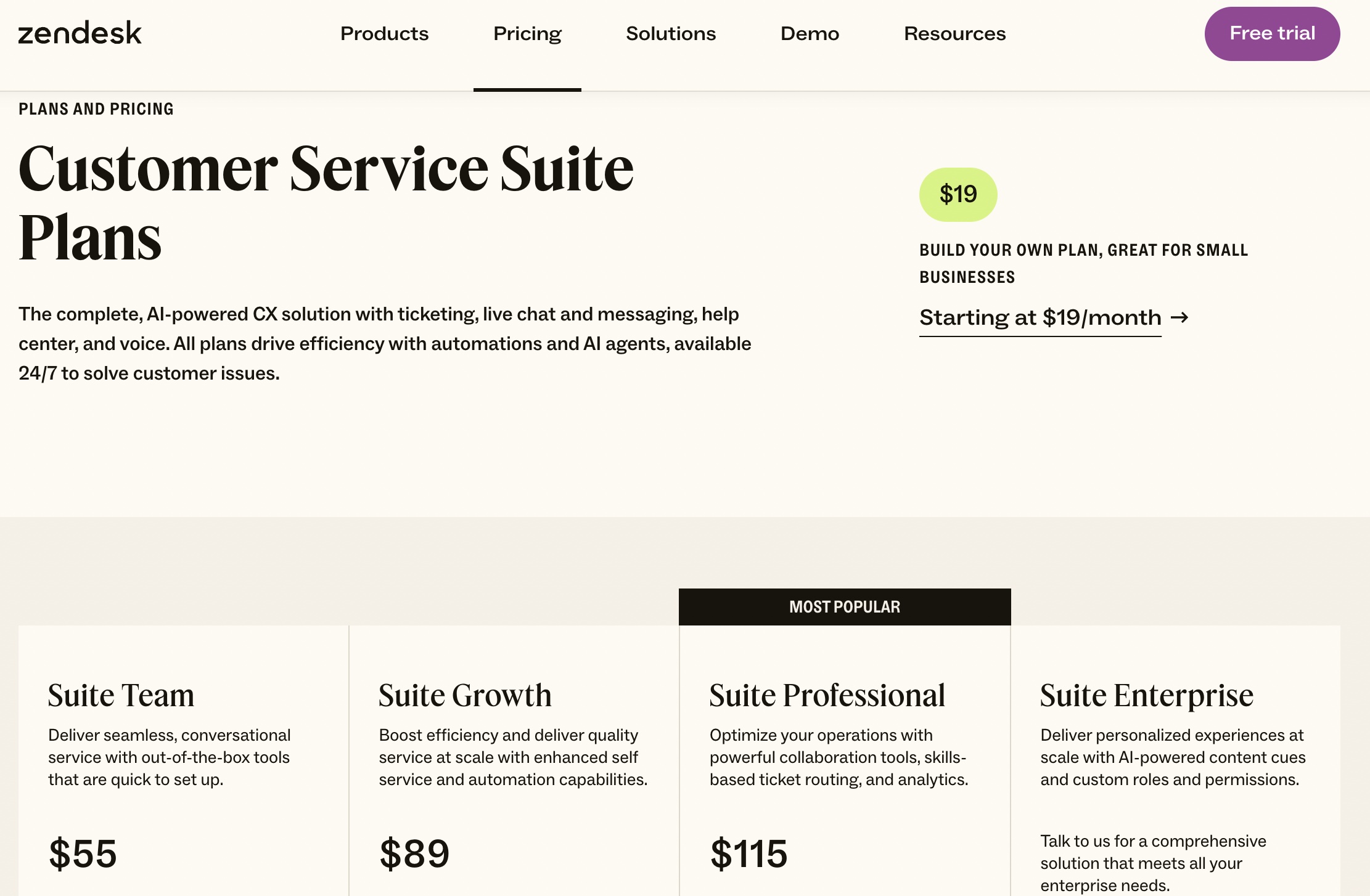

Zendesk operates on a recurring subscription model, offering businesses customer service, sales, and engagement tools. The pricing varies based on company size, features, and level of customization.

Main Subscription Offerings:

- Zendesk Suite – Full customer service platform (ticketing, chat, help desk, automation)

- Zendesk Sell – CRM designed for sales teams

- Enterprise Plans – Custom contracts for large companies with high-ticket deals

Why does this model work? Predictable revenue stream, higher revenue per deal, less reliance on constant new sign-ups.

2. AI-Powered Automation (New Growth Driver)

Zendesk has invested heavily in AI-driven customer service tools, allowing businesses to cut costs and improve efficiency.

AI Offerings That Generate Revenue:

- AI Chatbots – Handle customer inquiries automatically, reducing the need for human agents

- Predictive Analytics – Helps companies anticipate customer issues before they arise

- AI-Powered Self-Service – Customers get instant answers without speaking to an agent

Why is AI revenue is growing so fast? Companies want to cut support costs (AI reduces the need for human agents) and enterprise clients are willing to pay more for automation!

By 2026, AI-driven tools are expected to account for a much larger share of Zendesk’s revenue.

3. Professional Services & Consulting (Hands-On Enterprise Support)

Professional Services & Consulting accounts for 15% of Zendesk’s total revenue.

Unlike smaller customers who use Zendesk “out of the box,” large enterprises need custom integrations, dedicated account managers, and workflow automation.

How Zendesk Makes Money from Professional Services:

- Custom integrations – Tailoring Zendesk to fit complex business operations

- AI chatbot training – Helping companies train AI to match their support needs

- Dedicated support teams – White-glove service for high-ticket enterprise clients

Why does this matter? It increases customer retention, raises switching costs, and drives more subscription revenue!

While not Zendesk’s biggest revenue driver, professional services help land and keep enterprise clients—a major focus for the company’s growth.

4. Marketplace Revenue (Expected to Hit $200M+ by 2026)

Marketplace revenue is a smaller but rapidly growing revenue stream.

Zendesk has built an ecosystem of third-party apps and integrations that companies can purchase to extend the platform’s functionality.

How the Marketplace Makes Money:

- Third-party developers build apps (Zendesk takes a percentage of sales)

- Businesses pay for premium integrations (Salesforce, Slack, Microsoft Teams)

- AI-powered add-ons for automation, analytics, and security

Zendesk’s marketplace revenue is on track to surpass $200M by 2026, making it an increasingly important part of the business.

Zendesk vs. Competitors

Zendesk is a major player in the customer support software market, but it’s far from the only one.

Competitors are aggressively innovating, pushing AI automation, integrating with broader CRM solutions, and expanding into enterprise support at scale.

So, where does Zendesk stand in 2024, and how does it stack up against its biggest rivals?

Revenue Comparison: Where Zendesk Stands in 2024

Zendesk is currently generating $1.93 billion in annual revenue, a strong number that puts it ahead of many direct competitors—but still far behind the industry’s biggest heavyweight, Salesforce Service Cloud.

Here’s a breakdown of how Zendesk compares to its top competitors in customer service software revenue for 2024:

| Company | 2024 Revenue | Strengths |

|---|---|---|

| Salesforce Service Cloud | $8.6B | Deep enterprise CRM integration, AI automation |

| Zendesk | $1.93B | Strong brand, AI investment, expanding enterprise focus |

| HubSpot Service Hub | $1.5B | Popular with SMBs, strong marketing & sales integrations |

| Freshdesk (Freshworks) | $580M | Affordable pricing, solid automation for SMBs |

| Intercom | $300M | AI-powered customer engagement, strong chatbot capabilities |

| Zoho Desk | $240M | Cost-effective, widely used in international markets |

While Zendesk holds the second position, its revenue is less than 25% of Salesforce’s Service Cloud business. However, it is far ahead of other competitors like Intercom, Freshdesk, and Zoho Desk.

But revenue alone doesn’t tell the whole story—each of these competitors is targeting a different segment of the market.

1. Salesforce Service Cloud ($8.6B): The Enterprise Giant

Dominating the enterprise customer support space is Salesforce, with its Service Cloud generating over $8.6 billion annually—more than four times Zendesk’s revenue.

What makes Salesforce so dominant?

- Deep integration with Salesforce CRM – Most large enterprises already use Salesforce for sales and marketing, so adding Service Cloud is a natural extension.

- AI-Powered Automation – Salesforce has integrated Einstein AI into its support workflows, making its automation tools more powerful than ever.

- Strong Enterprise Sales Teams – Salesforce’s massive B2B sales force ensures it stays deeply embedded in enterprise ecosystems.

Why Zendesk can still compete:

- Better user experience and faster implementation – Salesforce is often seen as complex and resource-heavy, while Zendesk is easier to set up.

- More agile AI features – Zendesk is focusing on AI-driven chatbots and predictive analytics, which could appeal to enterprises looking for faster innovation.

However, Zendesk will have to fight hard to win large enterprise contracts since Salesforce already has deep relationships with many Fortune 500 companies.

2. HubSpot Service Hub ($1.5B): The SMB and Mid-Market Challenger

HubSpot’s Service Hub has grown quickly, reaching $1.5 billion in revenue in 2024. Its main advantage? Tight integration with HubSpot’s marketing, sales, and CRM tools.

Strengths of HubSpot Service Hub:

- Popular with SMBs and mid-market companies – Many small businesses already use HubSpot’s CRM and can seamlessly add its Service Hub.

- Inbound Marketing Powerhouse – HubSpot’s massive content marketing strategy keeps pulling in new users organically.

- Lower price point than Zendesk – HubSpot’s pricing is often more affordable for growing businesses.

How Zendesk compares:

- Stronger focus on AI and automation – HubSpot isn’t as advanced in AI-driven customer support.

- More enterprise flexibility – HubSpot is still mostly SMB-focused, while Zendesk is aggressively moving upmarket.

HubSpot’s Service Hub is growing fast, but it doesn’t yet threaten Zendesk’s dominance in enterprise support.

3. Freshdesk (Freshworks) – $580M: The Budget Alternative

Owned by Freshworks, Freshdesk is a strong competitor in the lower-cost customer support space, bringing in $580 million in revenue in 2024.

Freshdesk’s advantages:

- Affordable pricing for SMBs – Freshdesk is significantly cheaper than Zendesk, making it a go-to choice for startups.

- Decent AI-powered automation – Freshdesk has strong AI features, though they aren’t as advanced as Zendesk’s.

- Flexible support options – Offers a mix of chat, email, and ticketing solutions for small businesses.

Where Zendesk has the edge:

- Stronger enterprise focus – Freshdesk is still mostly used by small businesses, whereas Zendesk is now targeting large enterprises.

- More AI-driven features – Zendesk’s AI-powered chatbots and automation tools are more sophisticated.

- Better marketplace integrations – Zendesk’s app marketplace is more developed, allowing for more customization.

Freshdesk will continue to grow, but it’s unlikely to steal Zendesk’s high-value enterprise clients.

4. Intercom ($300M): The AI Disruptor

One of the biggest threats o Zendesk is Intercom, despite being a smaller company with $300 million in revenue. Its primary advantage? AI-powered automation.

Why Intercom is gaining ground:

- AI-driven messaging and chatbots – Intercom focuses on proactive customer engagement, not just support.

- Deep automation capabilities – Intercom’s bots handle complex workflows, reducing support costs for businesses.

- Modern, startup-friendly branding – Many fast-growing tech companies prefer Intercom over Zendesk.

Where Zendesk has the advantage:

- Stronger brand recognition in enterprise markets – Intercom is still growing, while Zendesk is already trusted by major companies.

- More complete customer support ecosystem – Intercom is strong in live chat and AI messaging but lacks Zendesk’s full suite of support tools.

- Larger revenue and market penetration – Zendesk is more than six times larger in revenue, giving it more resources to expand.

Intercom is growing fast, but it hasn’t yet broken into large-scale enterprise support, where Zendesk has a stronghold.

5. Zoho Desk ($240M): The Low-Cost Global Player

Even though Zoho Desk is the cheapest alternative on this list ($240 million in revenue in 2024), they popped up as #1 on Google when I searched for most of its competitors!

It’s widely used in international markets, particularly by small businesses in India, Southeast Asia, and Latin America.

Zoho Desk’s strengths:

- Extremely low cost – Zoho Desk is one of the cheapest helpdesk tools available.

- Built-in integrations with Zoho CRM – Many Zoho CRM users choose Zoho Desk because of its seamless compatibility.

- Growing AI features – Zoho has been investing in AI, though its tools are still less advanced than Zendesk’s.

Where Zendesk wins:

- More robust enterprise features – Zoho Desk is not built for large enterprises, while Zendesk is.

- Better customization and marketplace options – Zendesk has a stronger third-party app ecosystem.

- More premium AI-powered automation – Zendesk’s AI tools are far more advanced.

Zoho Desk is a strong low-cost competitor, but it’s unlikely to challenge Zendesk in high-end customer support solutions.

So, Can Zendesk Win the Long Game?

Zendesk is in a strong position, ranking second only to Salesforce Service Cloud in total revenue. It has successfully moved into the enterprise space, is expanding its AI capabilities, and is growing its marketplace ecosystem.

However, competition is tougher than ever. Salesforce remains the dominant force in enterprise support, while AI-first companies like Intercom and Drift are pushing hard into automation.

To keep growing, Zendesk must continue investing in AI-driven automation, secure more enterprise contracts, and expand its app marketplace. If it can execute well, it has a real shot at surpassing $3.4 billion in revenue by 2025.

But if it loses ground in AI or fails to retain enterprise customers, competitors are ready to steal market share. The next two years will determine whether Zendesk solidifies its position—or falls behind.

The $10.2 Billion Buyout: What Happened?

In 2021, Zendesk was at its peak. Revenue had surged to $1.34 billion, growing 30% year-over-year, fueled by strong enterprise adoption and AI-driven automation.

Investors were confident, and the company was expanding aggressively. Zendesk was hiring at record pace, launching new features, and positioning itself as the dominant player in customer support software.

But within a year, things took a sharp turn.

By mid-2022, Zendesk’s stock had dropped 45%, and its leadership was under attack. Activist investors accused the company of mismanagement, failing to maximize shareholder value, and making costly strategic mistakes.

A high-profile $4.1 billion acquisition attempt of SurveyMonkey (Momentive) collapsed, shaking investor confidence even further.

Months later, private equity firms Hellman & Friedman and Permira acquired Zendesk for $10.2 billion, taking it off the public market. The once-thriving SaaS giant was now in the hands of private owners, shifting its focus toward profitability over aggressive expansion.

Zendesk’s Stock Collapse and Investor Pressure

At the start of 2022, Zendesk was still seen as one of the strongest SaaS brands in customer support software.

But the broader tech industry was shifting.

Investors who had once rewarded high-growth software companies—even those operating at a loss—were now demanding profitability over pure expansion. Zendesk, despite its strong revenue growth, wasn’t seen as profitable enough.

As the stock declined, activist hedge fund Jana Partners stepped in.

They argued that Zendesk’s leadership was overspending, failing to maximize shareholder value, and ignoring the need for profitability.

They tried to strengthen the company through a $4.1 billion acquisition of Momentive. The deal was supposed to bring in advanced analytics capabilities and push Zendesk further into AI-driven customer support solutions. But investors hated the move. Many believed it was an unnecessary distraction from Zendesk’s core business.

Shareholders voted against the deal, and by February 2022, Zendesk was forced to walk away from the acquisition. The failed deal further weakened investor confidence, and with no other major growth strategy in place, pressure to sell the company only increased.

The Private Equity Takeover

By mid-2022, Zendesk’s board had little choice but to explore a sale.

The company’s stock had fallen to under $80 per share, a major drop from its previous highs. In June 2022, private equity firms Hellman & Friedman and Permira finalized a $10.2 billion buyout, taking Zendesk private.

For many investors, the sale was disappointing. Just a year earlier, Zendesk had been valued at $17 billion—now it was selling for significantly less.

But for Zendesk, the move provided an opportunity to reset. No longer burdened by public market scrutiny, the company could now focus on long-term strategy without the constant pressure of quarterly earnings reports and activist investor demands.

Zendesk’s Current Valuation and Market Position

Before the buyout, Zendesk had a public market valuation of $17 billion.

Today, private market estimates put its value at around $9.6 billion. As a private company, Zendesk now operates under a different set of expectations.

What Private Ownership Means for Zendesk

Under private equity ownership, Zendesk’s playbook has changed. The focus is no longer on hyper-growth at any cost. Instead, the goal is profitability, efficiency, and long-term scalability.

With private equity backing, Zendesk is now streamlining its operations. Cost-cutting measures are expected, particularly in areas like marketing, sales, and underperforming product lines. The company is prioritizing enterprise contracts over SMB customers, betting that long-term, high-value clients will stabilize its revenue streams.

At the same time, Zendesk is making aggressive moves into AI-powered automation. Chatbots, predictive analytics, and self-service tools are becoming essential in modern customer support, and Zendesk needs to stay ahead of AI-native competitors like Intercom and Drift. Unlike before, when the company had to justify every new investment to Wall Street, it now has the flexibility to double down on AI without immediate investor pushback.

However, private ownership also comes with challenges. Zendesk no longer has access to public capital markets, meaning it must fund its own growth through internal cash flow and private investments. If the company wants to make major acquisitions or invest heavily in AI, it will need to do so with more financial discipline than before.

The pressure is still there, just in a different form. Private equity firms typically aim to exit their investments within five to seven years, either by selling the company to another buyer or taking it public again at a higher valuation. This means Zendesk’s leadership has a limited window to prove that the company can become significantly more profitable and valuable.

What Next?

Zendesk’s $10.2 billion buyout was more than just a financial transaction—it was a complete shift in strategy. The days of aggressive spending and high-risk expansion are over. Instead, the company is now focused on efficiency, AI-driven automation, and locking in high-value enterprise clients.

Despite the challenges, Zendesk has ambitious goals. The company has set a target of reaching $3.4 billion in revenue by 2025, nearly doubling its current revenue in just three years. Whether it can achieve this depends on how well it navigates the competitive landscape, improves its profitability, and expands its AI capabilities.

For Zendesk, the next few years will determine whether this private equity reset was a new beginning or just a temporary lifeline.

How Zendesk Plans to Stay Ahead

Zendesk is at a pivotal moment in its history. After reaching $1.93 billion in revenue in 2024, the company is now pushing aggressively toward an ambitious $3.4 billion revenue target by 2025. The question is: can it get there?

The customer service landscape is evolving rapidly, driven by AI automation, enterprise software consolidation, and increasing competition from niche players. Zendesk no longer just competes with traditional helpdesk solutions—it now has to fend off AI-native startups like Intercom and Drift, as well as enterprise behemoths like Salesforce and Microsoft.

To maintain its dominance, Zendesk is focusing on three core strategies: expanding its enterprise business, enhancing AI-powered automation, and building a stronger marketplace ecosystem. These initiatives are designed to reduce customer churn, increase revenue per client, and solidify Zendesk’s position as the go-to platform for high-growth businesses and global corporations alike.

But executing these strategies won’t be easy. The challenges ahead are just as significant as the opportunities.

Enterprise Expansion: Moving Upmarket and Reducing Churn

Zendesk’s early success was built on small and mid-sized businesses (SMBs). The company’s intuitive interface, quick setup process, and affordable pricing made it a favorite among startups and tech companies. But as Zendesk scaled, it became clear that SMBs had a major downside—churn.

Unlike large enterprises, SMBs have less predictable revenue, fewer resources for long-term contracts, and a higher likelihood of switching software. This meant that Zendesk had to constantly acquire new customers just to maintain its revenue base.

Over time, the company recognized that enterprise clients provided more stability, larger contract values, and higher retention rates. Instead of dealing with thousands of small accounts, Zendesk could focus on winning high-value, multi-year contracts from large corporations.

By 2024, this strategy had paid off. More than 50% of Zendesk’s revenue now comes from enterprise clients, a huge shift from 2017, when SMBs accounted for 70% of its sales.

However, moving upmarket isn’t just about increasing contract sizes—it requires a fundamental shift in how Zendesk operates. Large enterprises demand customization, advanced security, deep integrations, and dedicated account management. Zendesk has responded by:

- Expanding its salesforce to focus specifically on enterprise accounts

- Building out a professional services division to assist with implementation and onboarding

- Enhancing security and compliance features to meet the needs of highly regulated industries

- Developing AI-powered automation tools that allow large teams to handle support tickets at scale

But moving into the enterprise space also means facing new challenges. Zendesk now competes directly with Salesforce Service Cloud, HubSpot, Microsoft Dynamics 365, and Oracle CX—companies that already have strong relationships with Fortune 500 firms.

To stand out, Zendesk must prove that it can provide better automation, a more seamless user experience, and stronger customer insights than its competitors. This is where AI becomes critical.

AI and Automation: Enhancing AI Chatbots and Predictive Analytics

AI has transformed customer support from a human-powered operation into a hybrid model where automation handles a growing share of interactions. In today’s world, businesses no longer want to just manage customer service—they want to eliminate inefficiencies, predict problems, and resolve issues before customers even reach out.

Zendesk is betting big on AI, investing heavily in automation, predictive analytics, and self-learning chatbots.

Smarter Chatbots

Zendesk’s AI chatbots already handle basic customer inquiries, but the next step is making them more intelligent and autonomous. The goal is for AI to not just respond to questions but to:

- Understand the intent behind customer messages and generate more personalized responses

- Handle multi-step interactions without human involvement

- Offer proactive solutions before customers even ask

For enterprises, this means lower support costs, faster resolution times, and better customer satisfaction.

Predictive Analytics for Proactive Support

Instead of simply responding to tickets, Zendesk’s AI will be able to anticipate customer issues before they happen. By analyzing past interactions, customer behavior, and product usage trends, Zendesk’s system will:

- Identify frustrated users before they churn

- Alert businesses to recurring product issues

- Offer automated suggestions and fixes before customers submit a ticket

This level of predictive customer service reduces support volume, improves retention, and strengthens long-term customer relationships.

Seamless AI-Human Handoffs

AI is powerful, but it can’t replace human agents entirely. Zendesk is building more advanced AI-human collaboration features to:

- Ensure complex issues are escalated to human agents without losing context

- Allow agents to take over conversations without disrupting the customer experience

- Use AI to suggest responses and guide agents in real time

By balancing automation with human expertise, Zendesk aims to maximize efficiency while maintaining a high-quality customer experience.

However, AI-first companies like Intercom and Drift are aggressively pushing into Zendesk’s market, and Salesforce is integrating more AI capabilities into its Service Cloud offering. If Zendesk doesn’t move fast enough, it risks falling behind in the AI arms race.

Marketplace Growth: Expanding Third-Party Integrations

Beyond AI, Zendesk is also focusing on growing its marketplace ecosystem.

The Zendesk Marketplace allows businesses to purchase third-party integrations, AI-powered tools, and automation add-ons. By 2026, Zendesk’s marketplace revenue is projected to exceed $200 million annually.

A strong marketplace benefits Zendesk in multiple ways:

- It increases customer stickiness—Once companies integrate Zendesk with dozens of third-party tools, switching platforms becomes much harder.

- It generates recurring revenue—Many marketplace apps operate on a subscription model, meaning Zendesk earns a cut of each sale.

- It attracts AI developers—As AI becomes more central to customer support, Zendesk wants external developers to build specialized AI tools for its platform.

The challenge? Competing against Salesforce’s massive app ecosystem. Zendesk must attract developers, expand its marketplace offerings, and provide businesses with more customization options to remain competitive.

Will Zendesk Hit $2 Billion in 2025?

With $1.93 billion in revenue, Zendesk is likely to cross the $2 billion mark by early 2025. However, reaching $3.4 billion within the same year is an entirely different challenge.

Several risks could slow down Zendesk’s growth:

- AI Disruption – If AI-native competitors move faster, Zendesk could lose market share to companies like Intercom and Drift.

- Enterprise Adoption Delays – Large businesses don’t switch software overnight. Zendesk needs to speed up its sales cycle and prove its value to win big contracts.

- Customer Churn – If Zendesk fails to differentiate itself, enterprise customers could switch to Salesforce, Microsoft, or newer AI-driven platforms.

While hitting $2 billion in revenue is likely, getting to $3.4 billion will require flawless execution.

Can Zendesk Keep Dominating?

Zendesk has built a powerful brand and a strong foundation in customer support software. Its focus on enterprise expansion, AI-powered automation, and marketplace growth positions it well for the future.

But the challenges ahead are significant. Competition is fierce, AI-native companies are moving fast, and enterprise customers have more choices than ever.

The next few years will be the true test of Zendesk’s ability to stay ahead in an evolving industry. If it successfully executes its strategy, innovates in AI, and expands its marketplace ecosystem, it has a clear path to long-term dominance.

If it doesn’t, it risks being overtaken by faster, smarter competitors. The next 24 months will determine whether Zendesk remains the leader in customer support software—or becomes just another player in an AI-driven market.